|

|

|

Home

The first recorded tax legislation for the Massachusetts Bay Colony took place in November 1645. It stated that:

every male within this jurisdiction, servant & other, of the age of 16 years & upwards, shall pay yearly into the common treasury the sum of 20d, and so in proportionable way for all estates, viz.: that all and every person that have estates shall pay one penny for every 20s. estate, both for land and goods, & that every labourer, artificer & handicrafts man usually takes in summer time above 18d./day, shall pay per annum 3s. 4d. into the treasury over and besides the 20d. before mentioned, and all others not particularly herein expressed, as smiths of all sorts, butchers, bakers, cooks, victuallers, & company, according to their returns and incomings, to be rated proportionably to the produce of the estates of other men... (Nathaniel B. Shurtleff, ed., Records of the Governor and Company of the Massachusetts Bay in New England, 5 vols. [Boston, 1853-1854] III 088).This legislation, however, contained a major weakness. Because landholders held the most visible estates they were more heavily taxed compared with merchants whose riches, in the form of trade goods, were often not as accessible for valuation. In an attempt to remedy this discrepancy the colony enacted a law in 1651: that all merchants, shopkeepers, and factors shall be assessed by the rule of common estimation, according to the will and doome of the assessor in such cases appointed, having regard to their stock and estate, be it presented to view or not, in whose hands soever it be, that such great estates as come yearly into the country may bear their proportion in public charges... (Shurtleff IV 038). For a while this legislation seemed to have quietened real estate holders, but by 1668 they were complaining again, this time over the question of taxing imported commodities. To satisfy their concerns a new law was enacted in that year to ensure a fairer distribution of taxes. It ordered that two persons were to be appointed in the seaports of the colony:

who from time to time in their several towns shall repair to all warehouses, or other places where any foreign goods or commodities are put on shore in any of our harbours, or are sold or retailed on board any ship, shallop, or other vessel, & require of the merchant, owner, or other retailer thereof the sight of his invoices or other just & true account of their goods imported by them... [the commissioners] are authorized and empowered to assess such merchant or other trader or traders ... and accordingly shall give warrant to the constable of the town to levy on them one penny per pound to be paid into the public treasury, as the law requires (Shurtleff IV 364).This legislation seems to have satisfied those concerned for there were no other significant changes in the tax laws of the colony for at least the next fifty years. Salem Tax Lists Each male resident of the colony 16 year of age or older was required to pay three kinds of taxes to the province - a poll or head tax, a real estate tax and a personal tax. The real and personal taxes were assessed on the real estate and personal wealth a person owned. The poll tax, however, was assessed to all equally. Until 1697 the tax lists were required to show only the sum of these three taxes and therefore the yearly lists showed only one column for the total taxes paid. In 1697, however, the colony enacted legislation requiring those who collected the annual taxes to divide the lists into four columns; poll tax, real estate tax, personal tax, and the total of the three. (Shurtleff II, 302) The Salem tax lists have survived for the year 1683 and then for every year from 1689 to 1771. These lists were subdivided into wards, but the boundaries and number of wards varied over time depending upon the shift in the town's population. In 1683 there were five wards, by 1692 there were seven, and by 1715 there were eight. It remained that number until 1752 when four wards split from Salem to become the separate community of Danvers. We collected tax data from these lists for the year 1683 and for every fifth year from 1690 to 1770. In particular, the data in the total tax column for each household head was entered into a database along with the ward in which he or she resided. In all there were over fourteen thousand entries. Although the taxes in the lists were denominated in pounds (£), shillings, and pence, we converted these values into pence before entering them into the database. Thus £1 would be entered as 240 pence. This had the advantage of having all taxes converted to whole numbers and made sorting much easier. Once the data had been entered for any one year, it was sorted in descending order and divided into ten equal sections or deciles. The top decile was given the numeric value of one, and those who paid taxes in that decile were assumed to be among the wealthiest ten percent in Salem. Conversely, the bottom decile was given the numeric value of ten, and those who paid taxes in that decile were assumed to be among the poorest ten percent in the town. Returning to the original documents, the tax lists for all eighteen years were searched to find both the wards and taxes paid by all seafarers and their relations. In each case his or her total tax was converted from pounds (£), shillings, and pence to pence. This value was found in the database and the person's name entered beside it. In this way we were able to determine for each individual the appropriate decile rating for that year. It is these ratings we are referring to whenever a decile value is mentioned in Young Men and the Sea.

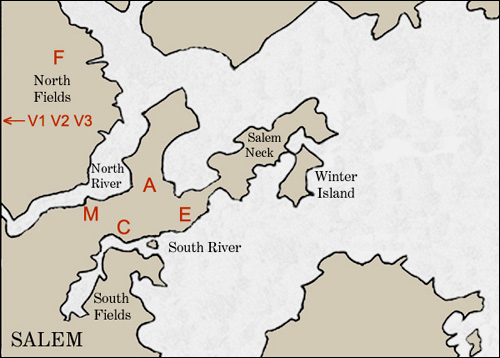

We assigned each ward a letter based on some distinguishing characteristic that we first noticed when we examined the tax lists of 1683. E ward covered the waterfront area of Salem, and was named after Philip English, a major shipowner, who collected the taxes in that ward in 1683. We thought many merchants dwelled in M ward, and believed large numbers of artisans and craftsmen lived in A and C wards. F ward included the area called the north fields, a farming area located between the town and Salem Village. Finally V1,V2 and V3 referred to the area around and including Salem Village. (It was F, V1,V2 and V3 wards that became the town of Danvers in 1752.) Later we realized these characteristics did not hold up as tightly for several of the wards as we had first imagined, but by that time the letter codes had become firmly entrenched. In particular, we discovered that seafarers, who we thought lived primarily in E ward, had spread out into M, A and C wards. Merchants, artisans and craftsmen occupied all four wards in significant numbers. The data for each of the 18 years was converted into web page tables comprising five fields: Mariner, Taxes, Decile, Adj_Dec, and Year.

Salem Tax Valuation Lists Few complete tax lists for Salem survived after 1773, but another very useful type of document did. To determine the taxes each person was yearly required to pay, the town calculated the taxable wealth of each taxpayer and placed this information into tax valuation lists. Providing information on real estate and personal wealth, complete lists have survived for the town of Salem for the years 1761, 1774, 1777, and from 1784 to 1850. These lists were divided into four wards and assigned by the assessors the numeral values of 1 to 4. These were roughly equivalent to the letter values of E, A, C, and M assigned by us to the Salem tax lists. We compiled valuation tax data for 1777, 1785, for every five years following up to 1825, then 1829, 1834, 1840, 1845 and 1850 for a total of 15 years. Following the pattern of the assessors, we assigned the numbers 1, 2, 3, and 4 to the town's four wards. The Salem Tax Valuation Lists were also converted into web page tables, but this time they contained seven fields: Mariner, Ward, Polls, Taxable Real Estate Wealth, Taxable Personal Wealth, Taxable Total Wealth, Decile, and Year.

From 1683 up to and including 1794 both the tax lists and the tax valuation lists were denominated in pounds, shillings and pence. From 1795 onwards the lists were denominated in dollars and cents. Just as we converted pounds, shillings and pence to pence for the 1683 to 1790 period, from 1795 onwards we converted all values from dollars to cents. Vince Walsh Updated September, 2005 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

© 2003 - 2012 Maritime History Archive, Memorial University |